Alabama LLC

How to Start an LLC

Starting an LLC can be easy, it can be easier if you let us start one for you!

Fast & simple online LLC formation with worry-free services and support to form accurately and on time, guaranteed! Starts at $0 + state fee and only takes 5-10 minutes

Create an LLC Today

Let our experts file your business paperwork quickly and accurately, guaranteed!

Last Updated: March 19, 2025

What is an LLC and how does it work?

LLC stands for “limited liability company”. It is defined as a business structure that is allowed by state statute that combining some elements of a sole proprietorship or partnership with aspects of a corporation. This unique classification, like a corporation, enables an LLC to be considered a separate legal entity, and its owners have limited personal liability for the business’s affairs (often called personal asset protection). The process includes registration formalities that vary by state. And like a partnership or sole proprietorship, an LLC offers flexibility and simple maintenance; there aren’t complicated requirements like establishing a board of directors, keeping minutes, or holding shareholder meetings. (see more on our LLC definition page).

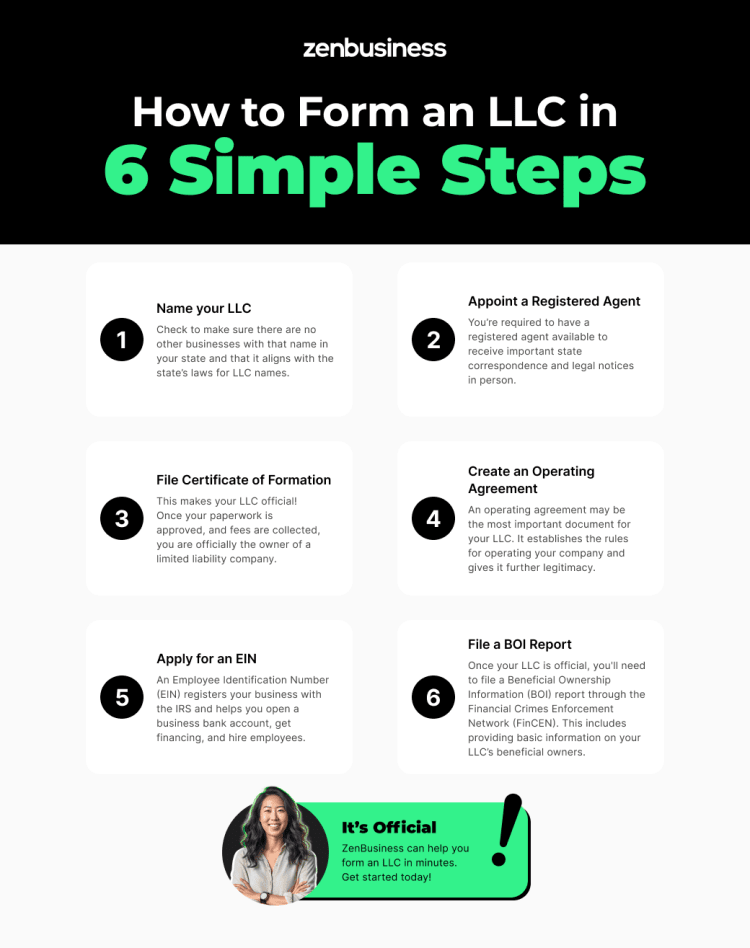

The 6 Steps to Starting an LLC

To start an LLC, you’ll need to choose a name for your business, select a registered agent, file Articles of Organization with the state, create an operating agreement, obtain an Employer Identification Number (EIN) from the IRS, pay any applicable state filing fees, and file a Beneficial Ownership Information report. LLC registration requirements vary state by state, so it’s important that you be well-versed in your specific state laws before proceeding. Generally, it comes down to these six basic steps in our guide below.

- Name your LLC

- Choose a registered agent

- File Articles of Organization for your state

- Create an LLC operating agreement

- Apply for an EIN and review tax requirements

- File a Beneficial Ownership Information report

Recommended articles:

Follow these steps to start an LLC:

1. Name your LLC

Now that you’ve decided you want to form an LLC, it’s time to bring your dream to life with its own name — and yes, it must be unique. When naming your LLC, you must choose something completely different from any other limited liability companies in your state.

The classification rules as to how different your LLC’s name must be from others vary from state to state. Although sometimes all it takes is switching up the punctuation or changing a word from singular to plural to qualify, it’s usually a smoother process when the names are more distinct. However, one component that is always required for the registration is the inclusion of “limited liability company” or an abbreviation of it at the end of the business name. The acceptable abbreviations also vary by state. For specific LLC State Guides select from below.

How to Get a limited liability company with a Unique Name

It’s important to do your research to check if your desired business name is available. Google is helpful, as is checking around on social media, but you will also want to complete a business database search on your Secretary of State website.

Your LLC name needs to be different from other LLCs in your state, and it also can’t be previously trademarked. There are two kinds of trademarks to be aware of: federal and state. Visit the U.S. Patent and Trademark Office (USPTO) site and search your business name or logo to make sure it hasn’t been federally trademarked.

Determining whether your desired business name already has a state trademark is trickier because many states don’t have a search engine for checking existing trademarks. Fortunately, the USPTO has a page linking to the office overseeing trademarks in each state. You can get started by contacting the appropriate office in your state.

Trademarking Names for LLCs

Once you’ve determined that it’s available to use, you have the option of registering your own trademark. A state trademark is less expensive and much less complicated to get; however, it does restrict your trademark benefits to the state it’s recognized in.

On the other hand, federal trademarks are more costly and can take longer to get, but you can use your trademark anywhere in the United States, and there is much more protection provided for your company. Federal trademarks also allow for the ® symbol, whereas state trademarks only allow TM (trademark) or SM (service mark). Trademarking your LLC can keep other businesses from using the same name or anything too similar.

Registering a DBA Name

There’s also an option to add a DBA name (“doing business as”) to LLCs. A DBA is just another name to call your business and can be very useful if your LLC offers multiple products or services. It can help differentiate between their specific business concerns.

Each state has different regulations when it comes to naming an LLC. You will often find that certain words are prohibited, including those that are considered profane or obscene or that may mislead people about the nature of the business. Some words are restricted in most states, such as “bank” and other forms of the word (“banking” and “banker”), “engineering,” “insurance,” and “savings.” In some states, business owners who wish to use words such as these must have a certain license and/or fill out additional paperwork.

You’ve spent time coming up with a name for your LLC and researching its availability — now you can think about securing it. Most states will allow you to reserve your desired name for a fee so that you don’t have to worry about someone else nabbing it before you can officially launch your business. Check with your state on the requirements to reserve your business name. Then, go one step further and reserve a domain name for your company website, so you have that set up and ready to go as soon as your business can launch.

Name your LLC

Enter your desired business name

2. Choose a registered agent

Your LLC needs to have a designated party — either a person or a business — who can receive legal notices (such as service of process for a lawsuit) and certain notices from the state. That business or individual is called a registered agent in most states, though they’re sometimes known as a resident agent, statutory agent, or an agent for service of process.

Having a registered agent is a requirement in the United States. Not having one could mean fines or even the dissolution of your LLC by the state. In addition to legal penalties for being out of compliance, failing to maintain an agent could mean that a process server can’t find you to notify you of a lawsuit. In that scenario, a court case against you could go forward without your knowledge, meaning you wouldn’t even have a chance to defend yourself.

You can be your own registered agent so long as you have a physical street address in the state in which your LLC is filed (P.O. boxes aren’t allowed); however, hiring an outside registered agent service has its benefits.

One drawback of being your own registered agent is the increased likelihood of receiving embarrassing legal documents in front of patrons. Not only can this be humiliating, but it might also damage confidence in your business. Using a separate registered agent at another location can help you avoid these risks.

Another drawback to being your own registered agent is that it takes the flexibility out of your day. Registered agents need to be constantly present at the registered office during normal business hours. If you’re tethered to the office, this means you have less time to take business meetings, attend working events, scope out opportunities, etc. A separate registered agent frees you from this responsibility.

*SPECIAL OFFER: $99 + state fees for the first year when you switch to ZenBusiness! Renews at $199/yr.

3. File the Articles of Organization in your state

The official name for the paperwork filed to register your business depends on which state you’re filing it in. Generally, the document is referred to as the Articles of Organization, but some states refer to it as a Certificate of Formation or Certificate of Organization. Regardless of what it’s called, the concept is the same: It’s used to establish state recognition of the LLC and outline the details of its members.

Filing Requirements for LLCs

Check your Secretary of State’s website to see the filing requirements, as these also vary state by state. You’ll always need basic information about the LLC and its members, including the LLC name and mailing address and the registered agent’s name and address. You might also be asked to state the purpose of the LLC and list any current LLC members and/or managers.

A few parts of the form might be unfamiliar to someone who is just entering the business world. You may be asked whether your LLC is member-managed or manager-managed. In a member-managed LLC, the members take it upon themselves to handle day-to-day operations and decide who’s responsible for what. In a manager-managed LLC, one or more supervisors are chosen by the members to be in charge. As an LLC member, you have the flexibility to shape the management of your company. Whether you opt for a member-managed or manager-managed LLC, each member plays a pivotal role in steering the business towards success.

You’ll also need to list the location of operations, which should be the place in which members work together. If the business is operated from a private home, list your home address. If mail is not deliverable to the place of work, make sure to include a USPS-verified mailing address.

The final, and most important, step is having an organizer of the LLC sign the form. Then, you’re all set to submit it. In most states, this can be done online or by mail. Any instructions for submitting the signed form and payment can be found on your Secretary of State’s website.

4. Create an LLC operating agreement

Although LLC operating agreements are not required in every state, it’s a smart business move to have one. This legally binding document provides clear and concise definitions of all ownership terms and rules or management decisions. An operating agreement protects owners’ personal assets and outlines ownership percentages, responsibilities, voting power, and a succession plan if an owner decides to leave the business.

Having an operating agreement can prevent any miscommunication and resolve any conflicts between members. It’s not required by law to file an LLC operating agreement with the Secretary of State, so once all parties have agreed upon the terms and signed it, it’s advisable to keep the document safe and secure with other important paperwork.

Create an operating agreement online

Utilizing an operating agreement template for your LLC can set you up for success regarding having the right business structure and format for this important document.

5. Apply for an EIN and review tax requirements

After officially forming your LLC, you should consider registering it with the federal government by applying for an Employer Identification Number (EIN) from the IRS.

An EIN is the business equivalent of a personal Social Security number and is required if your LLC has multiple members or any employees. It’s free to apply for a Federal Tax ID Number, a.k.a. Employer Identification Number, and it can conveniently be done on the IRS website. When done online, the EIN is issued immediately.

6. File a Beneficial Ownership Information report

Important Note: As of March 21, 2025, the Financial Crimes Enforcement Network (FinCEN) issued an interim final rule that removes the requirement for U.S. companies and U.S. persons to report beneficial ownership information (BOI) to FinCEN under the Corporate Transparency Act. This means the Beneficial Ownership Information Report is no longer required.

Once your LLC is official, you still have an important new federal obligation to fulfill: filing a Beneficial Ownership Information (BOI) report. Starting in 2024, most LLCs and many other small businesses are required to submit a BOI report to the Financial Crimes Enforcement Network (FinCEN). The BOI report is a requirement under the Corporate Transparency Act, enacted to enhance transparency regarding business ownership to prevent illicit financial activities. Entities subject to this rule include many limited liability companies (LLCs), corporations, and others formed by filing with a Secretary of State or a similar U.S. office. The report is meant to disclose information about a business’s “beneficial owners,” who are individuals with substantial control, ownership interest exceeding 25%, or significant economic benefit from the business’s assets.

You’ll first need to gather information on your LLC’s beneficial owners, including their full names, addresses, and identification documents. Then go to the FinCEN website, where you complete a form online or by PDF. There’s no fee to file.

Companies formed before January 1, 2024, must file their report by January 1, 2025. Those created after that date have 90 days from their approval by the state to file, and those formed after January 1, 2025, have 30 days from receiving notice of approval. Failure to file can result in substantial penalties, both civil and criminal, making timely submission crucial.

Exempt businesses include those registered under the Commercial Exchange Act, public utilities, governmental authorities, insurance companies, and financial institutions. A foreign company doing business in the U.S. is also considered a reporting company and must file a BOI report. Even if a business closes, it may still be required to file if it hasn’t formally dissolved. Compliance with these rules is crucial to avoid criminal and civil penalties and remain compliant with the Corporate Transparency Act.

You can get more information on the FinCEN website. If you need guidance following this new federal requirement, our Beneficial Ownership Filing service can help.

Compare our packages

Our customized packages meet the compliance, filing speed, and support needs of your new business in one place.

starter

![]() Basic

Basic

Covers all your required filings with the state, accuracy guaranteed.

$0

+ state fees

![]() Processes in 7 to 10 business days*

Processes in 7 to 10 business days*

- Standard filing service

- 100% accuracy guarantee

- Worry-Free Compliance offer**

pro

![]() Most Popular

Most Popular

Everything to start and protect your LLC and keep it compliant year-round.

$199/yr

+ state fees

![]() Processes in 1 business day*

Processes in 1 business day*

- Rush filing service

- 100% accuracy guarantee

- Worry-Free Compliance

- Operating agreement

- EIN

premium

![]() Best Value

Best Value

Get additional tools and expert support to start and grow your business online

$299/yr

+ state fees

![]() Processes in 1 business day*

Processes in 1 business day*

- Rush filing service

- 100% accurate filing guarantee

- Worry-Free Compliance (included)

- Operating agreement

- EIN

- Business document template library

- Domain name with privacy

- AI website builder

- Business email address

- Premium Support

*Processing times are based on receiving complete information. ZenBusiness processing times do not include Secretary of State processing times, which can vary.

**SPECIAL OFFER – Starter includes one optional free year of Worry-Free Compliance (renews at $199/yr).

More About Limited Liability Companies

Compare LLC to other business structures

Compare how LLCs stand in contrast to other business entities like corporations and partnerships.

Sole Proprietorship

Operating a business as a sole proprietor is relatively low-cost and straightforward, but the major difference between operating as a sole proprietorship versus an LLC is the separation between personal and business. Personal assets are kept separate in an LLC, whereas a sole proprietor’s personal and business expenses are the same. If someone sues the business, they can go after your personal savings and property.

Both LLCs and sole proprietorships benefit from pass-through taxation, avoiding double taxation.

Compare LLCs vs. sole proprietorships.

General Partnership

Here, you are dealing with formalities. Forming an LLC requires several specifics, including paperwork that is drafted and filed with the Secretary of State and paying the filing fee. When forming a general partnership with someone, it requires a much less formal agreement between the two parties. Like sole proprietorships, general partnerships have pass-through taxation.

Visit LLCs vs. Partnerships for a full comparison.

Limited Liability Partnership (LLP)

When it comes to personal liability, LLCs generally offer more broad protection than LLPs. With an LLC, members are usually not personally liable if the LLC is sued or owes any debts.

An LLP may offer limited liability in the same way as an LLC, but this depends on the state in which your business is formed. For example, in some states, an LLP only affords liability protection from other partners’ negligence, but you would still be personally liable for the business’s overall debts and financial obligations.

Some states also require at least one LLP partner to assume unlimited personal liability, while the other partners have limited liability. For this reason, it’s crucial that you check with the Secretary of State office in your state to learn about the specific rules and regulations.

Compare LLCs vs. LLPs in more detail.

C Corporation

C corporations (the default form of corporation) experience double taxation; profits are taxed at the corporate level and again when distributed as dividends to shareholders. LLCs, with their pass-through taxation, avoid this double hit.

C corporations have a structured management hierarchy with a board of directors and officers, while LLCs allow for more flexible management arrangements.

With a C corporation, you can sell stocks. This not only can help in raising funds, but it also makes ownership transfer easier. LLCs can’t sell stock, and transferring ownership of them can be complex.

Learn more about LLCs vs. C corps.

S Corporation

Rather than a business entity itself, an S corporation is a federal tax election. A C corporation or an LLC can apply to be an S-corp. An S corporation has pass-through taxation, but there are more restrictions for qualifying; for example, an S corp can have no more than 100 members.

Learn more about S corporations vs. LLCs.

What are the advantages and disadvantages of LLCs?

LLC Advantages

- Limited Liability: Your personal assets are generally protected from business debts and legal liabilities. If the business faces financial trouble or legal issues, your personal savings and property are usually off the hook.

- Pass-Through Taxation: By default, LLCs have pass-through taxation, which allows the profits and losses of the business to “pass through” to the individual members, who then report this income on their personal tax returns. This helps avoid the “double taxation” issue faced by C corporations, where profits are taxed at the corporate level and again at the individual level when distributed as dividends to shareholders. S corporations also have pass-through taxation.

- Flexible Taxation: You have the option to choose how you want your business to be taxed. By default, an LLC has “pass-through” taxation, where the business profits flow straight to your personal tax return without first being taxed at the business level (unlike most corporations). Alternatively, you can opt to be taxed as an S corporation or a C corporation, which can provide other tax benefits for certain LLCs.

- Simplified Paperwork: Compared to corporations, LLCs have less administrative burden. You won’t need to deal with regular meetings, detailed record-keeping, or complex decision-making processes. This simplicity saves time and effort.

- Credibility: Adding “LLC” to your business name can boost your credibility. It signals to clients, partners, banks, and investors that you’ve taken steps to establish a legitimate business structure, potentially enhancing trust and professionalism.

LLC Disadvantages

- Limited Life: In some states, the existence of an LLC may be terminated if a member leaves or dies. It’s easier for a corporation to exist in perpetuity.

- Self-Employment Taxes: While LLCs offer flexibility in taxation, they can also subject you to self-employment taxes. This can lead to higher tax payments compared to certain corporate structures.

- Complexity in Multiple States: If you plan to operate in multiple states, you may face additional paperwork and fees to register your LLC in each state. This can add complexity and costs to your business operations.

- Less-Established Structure: Compared to corporations, which have well-defined structures like boards of directors and shareholders, LLCs can be perceived as less established. This might matter when dealing with certain partners, investors, or clients.

- Limited Investment Opportunities: If you’re looking to raise substantial capital from investors or plan to go public, an LLC structure might not be the most suitable option. Corporations often offer more favorable options for these scenarios.

In a nutshell, forming an LLC comes with the perks of liability protection, tax flexibility, and simplicity. However, it’s important to consider potential limitations like limited life, self-employment taxes, and less-established structure. Assessing your business’s needs and goals will help you determine if an LLC is the right choice for you.

How much does the LLC application process cost?

Is an LLC free? Creating an LLC isn’t free, as it involves a range of costs that vary by state. Typically, the formation filing fees range between $50 and $500. This process can be accomplished either online using a credit or debit card, or by mail with a check or money order, through your Secretary of State’s website.

Beyond the initial filing fee, states may also mandate additional charges such as business license fees, publication fees, name reservation fees, and others. Moreover, an LLC carries recurring costs for its maintenance, including filing annual or biennial reports, renewing licenses and permits, and paying franchise taxes. These costs will all vary widely by state.

Types of LLCs popular with businesses

There are several different types of LLCs, each with its own entity characteristics and purposes. Here’s a breakdown of the main types:

Single-Member LLCs (SMLLC): A single-member LLC is owned and operated by a single individual (member) or entity. It’s the simplest type and offers limited liability protection for the owner (member). Taxes are usually reported on the owner’s personal tax return.

Multi-Member LLCs: A multi-member LLC has two or more owners (members). It’s great for businesses with multiple partners or investors. Each member’s share of profits, losses, and responsibilities is typically outlined in the operating agreement.

Series LLCs: Available only in a few states, a Series LLC can hold multiple “series” or subdivisions within one overarching entity. Each series can have its own assets, liabilities, and operations, providing some separation between them. This is useful for businesses with various ventures or properties.

Professional LLCs (PLLC): Certain licensed professionals like doctors, lawyers, accountants, and architects can form a professional LLC in some states. This structure doesn’t protect a member from malpractice claims against themselves, but it can protect them from malpractice claims against another member of the PLLC. This type of LLC is only available in certain states and for certain licensed professions.

Low-Profit Limited Liability Companies (L3C): An L3C is designed for businesses that aim to achieve a specific social or charitable goal while also making a profit. It’s a hybrid between a traditional LLC and a nonprofit, meant to encourage socially beneficial endeavors.

Foreign LLCs: This entity type applies when you form an LLC in one state but want to operate in another state. You’ll need to register your LLC as a foreign LLC in the state you want to do business in, complying with that state’s regulations.

Remember that the availability and regulations of these types of LLCs can vary depending on the state you’re in. It’s always a good idea to consult legal and financial experts to determine the best type of LLC for your specific situation and location.

What are the benefits of LLCs?

The benefits of an LLC include limited liability protection for personal assets, flexible tax options, simplified paperwork compared to corporations, and increased credibility.

Limited liability protection: One of the top perks of LLCs is that it usually shields your personal assets, like your house or savings, from business debts and liabilities. If the business runs into trouble or gets sued, your personal assets generally stay safe. It’s like having a protective bubble around your personal finances.

Flexible tax options: With an LLC, you get to choose how you want your business to be taxed. By default, an LLC has “pass-through” taxation, where the business profits flow straight to your personal tax return without first being taxed at the business level (unlike most corporations). Alternatively, you can opt to be taxed as an S corporation or a C corporation, which can provide other tax benefits for certain LLCs. This flexibility lets you adapt to your financial situation.

Simplified paperwork: Compared to corporations, which can have a mountain of paperwork and formalities, LLCs keep things refreshingly simple. You won’t need to deal with things like shareholder meetings or a board of directors. This means fewer administrative headaches and more time to focus on growing your business.

Increased credibility: Having “LLC” after your business name adds a level of professionalism and credibility. Clients, partners, banks, and investors tend to take you more seriously when you’re not just a sole proprietor. It shows that you’ve gone through the process of establishing a legitimate business structure.

Flexible Membership: LLCs offer a blend of flexibility in membership and management, standing as a middle ground between corporations and partnerships. LLCs can have an unlimited number of members, which can be individuals or other business entities, and can choose to be managed by selected members or outside managers. This flexible management structure, along with the freedom to distribute profits in any agreed manner among members, makes LLCs a less formal and more adaptable choice for entrepreneurs compared to the rigid structure and formalities associated with corporations.

So, when you put all these benefits together, forming an LLC can be a savvy move for your business. It provides protection, flexibility, simplicity, and credibility.

Entity Guidelines for States

The rules, procedures, and costs associated with forming an LLC can vary significantly from one state to another. Each state has its own set of statutes and regulations governing formation, operation, and dissolution. For instance, the filing fees for setting up an LLC can range from around $50 to $500 or more, depending on the state. Some states, like California, have additional annual taxes and reporting requirements that can add to the cost and administrative burden of operating an LLC. Moreover, the processing times for formation documents can range from a few business days to several weeks, depending on the state and whether expedited processing options are available and utilized.

In addition to varying costs, the level of information required and the procedures for forming an LLC may differ across states. Some states require a detailed list of member names and addresses, while others only require the name of a registered agent and the address of the LLC’s principal office. Furthermore, certain states may have unique naming conventions or restrictions and may require additional approvals for certain types of businesses. For example, New York requires LLCs to publish a notice of formation in two newspapers, which can significantly add to the cost and complexity of forming an LLC in that state. It’s important for entrepreneurs to carefully research and understand the specific LLC formation requirements and costs in their particular state to ensure compliance and to budget appropriately for the process.

Related articles:

Need help filing your LLC?

Do you need more help with starting your business? Our expertise is literally in helping new businesses form. We offer fast, accurate formation services online guaranteed. Our expert insights provide long-term business support to help you start, run, and grow your business.

State Guides for LLC Formation

Check out our comprehensive guides tailored to each state's LLC formation laws and processes.

Related Topics

LLC FORMATION THAT'S FAST AND SIMPLE

Take it from real customers

Very fast and exceptional service

Very fast and exceptional service! I am highly satisfied with my order and the level of communication from the company.

– Monique Bravo

The process was so quick and easy

The process was so quick and easy. They took care of everything and so promptly. I highly recommend Zen Business. I look forward to working with them…

– Griff Steadman

ZenBusiness saved the day!

ZenBusiness saved the day. I couldn’t be more pleased. I’m looking forward to letting Zen take care of all my business needs in the…

– Greyson Byers

Limited Liability Company (LLC) FAQs

-

It varies by state, but the standard time frame is two to three weeks from when the state receives your LLC documents, whether online or by mail. In some states, it can be expedited for an additional fee.

-

It’s usually best to form an LLC in the state where your business is located.

-

No. You can form an LLC by yourself. There is no requirement to use a lawyer.

-

If your LLC is filed as a corporation, you won’t need a 1099 for the business. However, if your LLC employs independent contractors, you will need to file 1099 forms for these individuals.

-

The steps may vary state to state, so check your state’s LLC dissolution procedures. Generally, the timeline is the same. You must file the Articles of Dissolution with your Secretary of State, and then file cancellations in any other states that your LLC does business in.

Next, you must file your final tax return, pay any final payroll taxes, and close your EIN. There’s a lot of paperwork and steps involved in the process.

-

Yes. Since an S corporation is a business entity, it can be the owner (or a member of) an LLC, but an LLC cannot own an S corporation — only individuals can own an S-Corp.

However, an LLC can be taxed as an S corporation if it meets an S corporation’s eligibility requirements, which include having a limited number of owners who are U.S. citizens.

-

Yes, but it’s not all that common. Certain requirements must be met, and it can be a little confusing to understand all of the legalities. It’s always wise to seek a legal and/or financial professional when considering these questions.

-

Yes, you can form your own limited liability company, provided you follow all of your state’s applicable laws. However, using our business formation service makes LLCs easy and inexpensive to form. We charge $0 to form your LLC, and then our business formation experts do the work for you and are there to answer your questions.

-

Piercing the corporate veil refers to a legal scenario where the courts set aside the limited liability protection normally afforded to members (owners) of an LLC, allowing creditors to go after the personal assets of the members to satisfy the debts of the LLC. This is a rare but serious situation that underscores a fundamental breach in the legal separation between the entity and its owners. It generally happens when the courts believe that the LLC is not truly a separate entity from its owners and that continuing to recognize it as such would result in fraud or an unfair outcome for the LLC’s creditors.

Several factors can contribute to a court’s decision to pierce the corporate veil of an LLC. Some of these factors include commingling of personal and business funds, failure to maintain separate financial records for the business, undercapitalization, failure to adhere to formalities required for LLCs, or using the LLC to perpetrate fraud or other wrongful conduct. By adhering to all required formalities, keeping personal and business finances strictly separated, and operating the LLC as a truly independent entity, owners can maintain the protective veil of the LLC and safeguard their personal assets from claims against the business.

-

Transferring ownership in an LLC and a corporation involves different procedures and implications due to their distinct structural frameworks. In an LLC, the transfer of ownership can be more complex and restrictive. Typically, the operating agreement of an LLC outlines the procedures and conditions under which ownership can be transferred. It may require the approval of all or a majority of existing members before a transfer can occur.

Additionally, the sale or transfer of membership interests may not automatically grant the transferee the rights to participate in the management of the LLC, unless the operating agreement provides for this or the existing members consent to it.

On the other hand, corporations have a more straightforward process for transferring ownership, especially in the case of publicly traded corporations. The shares of stock that signify ownership in a corporation are freely transferable on the open market, unless restricted by a shareholder agreement. The transfer of shares automatically confers both ownership and management rights to the transferee, making it a more fluid and less restrictive process compared to LLCs.

This ease of transferability in corporations facilitates the raising of capital and liquidity for shareholders. It’s one of the reasons why corporations are a preferred entity type for businesses that intend to go public or seek investments from a broader base of investors. The structured nature of corporations, with its clear delineation of roles and rights, makes them better suited for larger, more complex business operations with multiple investors and a broader ownership base.

-

A Certificate of Good Standing, also known as a Certificate of Existence or Certificate of Authorization in some states, is an official document issued by the state agency overseeing business registrations, typically the Secretary of State. It certifies that an LLC or another business entity is legally registered and compliant with the state’s requirements and regulations. The certificate validates that the LLC is up to date with its state filing requirements, fee payments, and any other mandated obligations in the state where it was registered.

An LLC might require a Certificate of Good Standing for various reasons. First, it’s often necessary when the LLC seeks to register or qualify to do business in another state, a process known as foreign qualification. Second, it may be required when an LLC is involved in certain financial transactions, such as securing funding from lenders or entering into contracts with other businesses. The certificate reassures the other parties that the LLC is a well-maintained, legitimate entity, adhering to state compliance requirements.

Additionally, if the LLC is looking to sell its business or merge with another entity, a Certificate of Good Standing will likely be required to confirm that the LLC is in a compliant status before proceeding with the transaction.

-

A foreign qualification is a legal process that allows an LLC or another business entity to operate and conduct business in a state other than the one where it was originally formed. When an LLC is formed, it’s automatically authorized to do business only in the state of its formation. However, if the LLC wishes to expand its operations to other states, it must obtain approval from each of those states by going through the foreign qualification process. This process typically involves filing specific documents with the Secretary of State or the relevant state agency, paying the necessary filing fees, and appointing a registered agent in the foreign state to receive legal and official communications on behalf of the LLC.

The necessity for foreign qualification arises when an LLC has a continuous and systematic presence or conducts business in a state other than its home state. This might include having a physical office, employees, bank accounts, or significant sales activities in the foreign state. The foreign qualification ensures that the LLC is compliant with the laws and regulations of the state where it seeks to do business. It also provides a legal platform for the LLC to enforce contracts and access the courts in the foreign state. Without foreign qualification, an LLC may face fines, back taxes, and other penalties, and may be denied the right to bring a lawsuit in the foreign state. Therefore, foreign qualification is a crucial step for LLCs planning to operate across state lines, helping ensure legal compliance and smooth business operations in each state.

“This is your life. You want to get it right.”

– Mark Cuban on Starting a Business*

Entrepreneur and Shark Tank host lays out 3 steps to follow when starting a business

* Mr Cuban has a financial interest in ZenBusiness

*Mr. Cuban has a financial interest in ZenBusiness and our affiliate partners may receive financial compensation for their support.

Disclaimer: The content on this page is for information purposes only and does not constitute legal, tax, or accounting advice. If you have specific questions about any of these topics, seek the counsel of a licensed professional.

ZenBusiness is a financial technology company and is not a bank. Banking services provided by Thread Bank, Member FDIC. The ZenBusiness Visa Debit Card is issued by Thread Bank pursuant to a license from Visa U.S.A. Inc. and may be used anywhere Visa debit cards are accepted. FDIC insurance is available for funds on deposit through Thread Bank, Member FDIC.

*Your deposits qualify for up to a maximum of $3,000,000 in FDIC insurance coverage when placed at program banks in the Thread Bank deposit sweep program. Your deposits at each program bank become eligible for FDIC insurance up to $250,000, inclusive of any other deposits you may already hold at the bank in the same ownership capacity. You can access the terms and conditions of the sweep program at https://thread.bank/sweep-disclosure/ and a list of program banks at https://thread.bank/program-banks/. Please contact customerservice@thread.bank with questions regarding the sweep program.

Ready to Start Your LLC?